Educate Yourself About The Affordable Care Act (Obamacare)

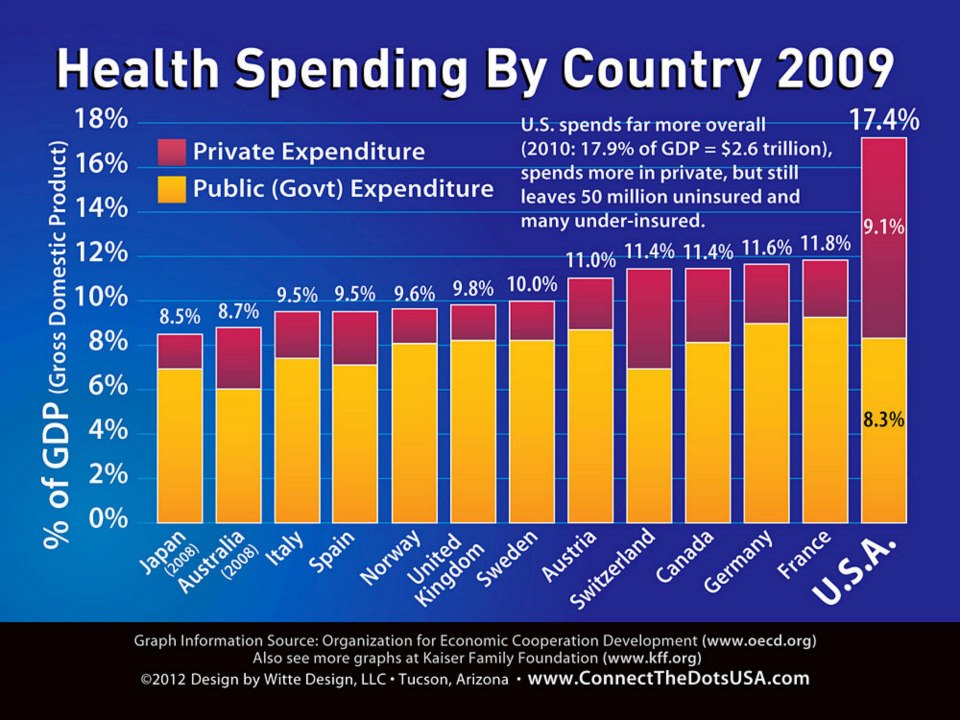

Compared to other developed countries, the U.S. spends far more overall. In 2009, that was 17.4% of our entire economy (GDP) or about $2.6 Trillion, with more than half coming from private spending. The next biggest spenders are France, Germany, Canada and Switzerland, which each spend about 11% to 12% of GDP and still manage to cover all their people. Taiwan set up its single-payer system from scratch in 1995, took its uninsured from 41% down to 8% within just the first year of operation, and now spends only 7% of its economy on healthcare with everyone insured. The Taiwanese, like the Japanese, go to the doctor on average 15 times/year compared to the U.S. average of 5 times/year. Patients have free choice of any hospital, clinic or doctor, so providers compete furiously for customers. When researching the developed world for the best healthcare model to follow, the Taiwanese quickly rejected America’s crazy quilt as a cautionary tale in what to avoid.

Illustration and commentary courtesy of Connect the Dots USA |

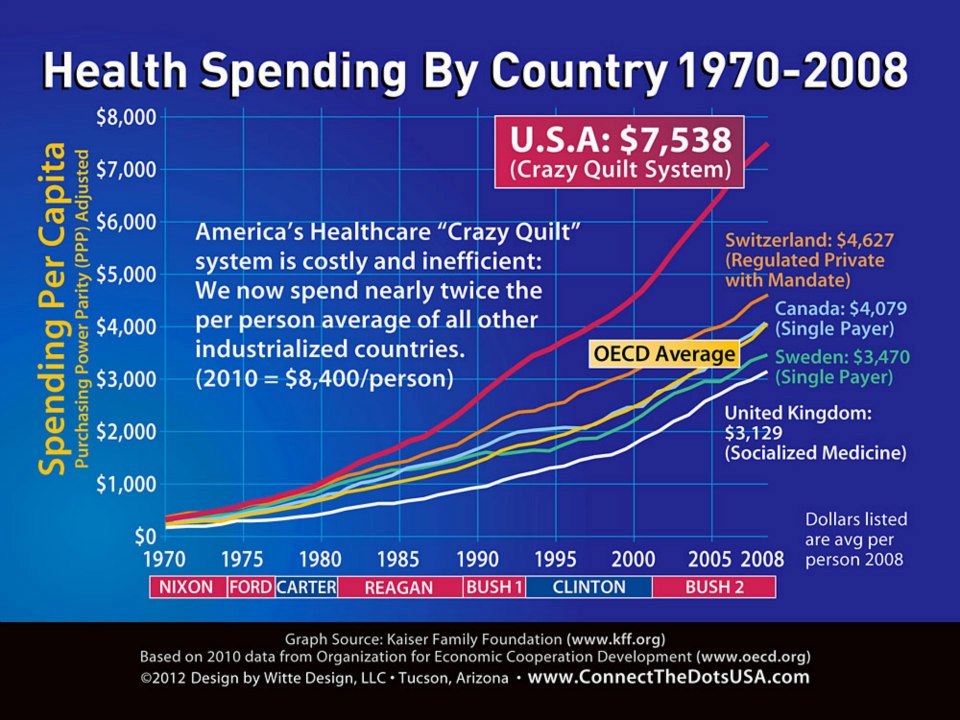

While average per capita health spending has gone up for every country in the last three decades, it has skyrocketed in the U.S. We now spend nearly twice the per person average of all other industrialized countries. In 2010, that was a whopping $8,400 per person.

Illustration and commentary courtesy of Connect the Dots USA |

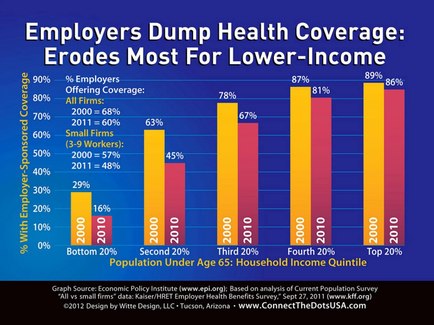

Even worse, in the last decade, many employers chose to dump healthcare coverage all together. This is especially true for lower-income workers — what I call the “Walmart” syndrome. It’s sad but true that rank-and-file Walmart employees often carry three cards in their wallet — a Walmart discount card, a food stamp card, and a Medicaid card. Walmart

epitomizes the growing number of employers that make taxpayers subsidize their bad business practices. In 2000, 68% of employers offered health coverage; in 2011, it was only 60%. For small firms, it’s even worse — dropping from 57% in 2000 to 48% in 2011. Illustration and commentary courtesy of Connect the Dots USA |

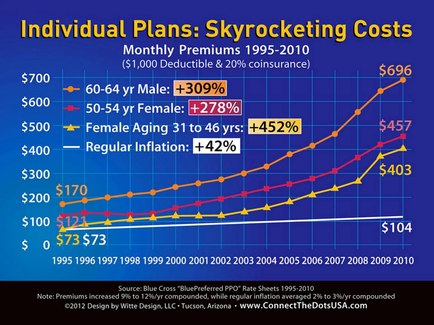

So workers and their families are then left to fend for themselves in the draconian world of non-group private insurance. Other than being uninsured, it doesn’t get much worse. First, if you’ve ever had any major illness like cancer, diabetes or a heart attack, don’t even bother applying. You’re too risky, and Big Insurance can’t make money off sick people! Ifyou’re lucky enough to qualify for a policy, they’ll probably exclude any body part that’s ever been treated. And, as you can see from these representative plots off my Blue Cross preferred rate sheets, brace yourself for double-digit premium increases every year. My $73 monthly

premium in 1995 had become $403 by 2010 (that’s with a $1,000 deductible and 20% coinsurance) — a whopping 450% increase in 15 years, far outpacing regular inflation. The older you are, the worse it gets. Illustration and commentary courtesy of Connect the Dots USA |

Do You Support Insurance Companies or American Citizens?

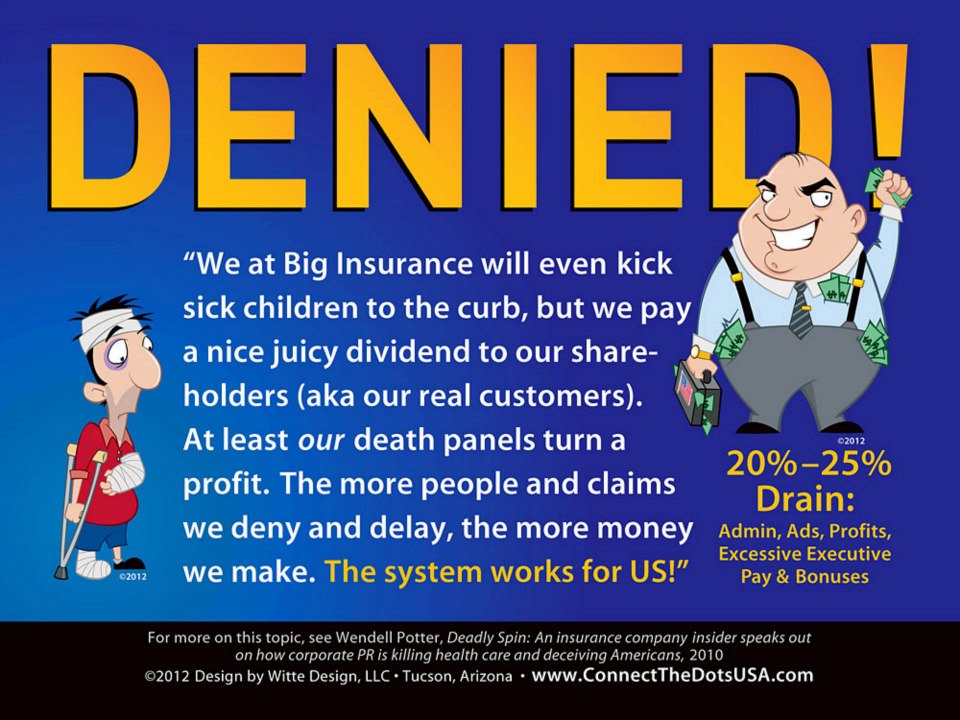

In addition to pre-existing condition discrimination and annually purging small businesses with sick employees, insurance companies regularly delay and deny claims or worse, cancel policies when individuals make a big claim. Unfortunately, greedy insurance companies answer to Wall Street’s relentless profit expectations and not to the medical needs of their

policy holders (aka their hostages). Through the unconscionable practice of “post-claims underwriting,” the insurance company scours your original application to find any little, even unrelated, medical thing you failed to mention to justify cancelling your policy. In 1993, an average 95 cents out of every private premium dollar was spent on actual medical claims (what Wall Street calls the “medical loss ratio”); now it’s down to 78 cents and continually dropping. American-style private insurance is an evil system built and sustained on greed. And Big Insurance is a useless middleman that drains 20 to 25 cents out of every premium dollar for paperwork, underwriting, advertising, lobbying, profits and excessive executive pay and bonuses. In 2007, the CEOs at the 10 largest publicly traded health insurance companies got an average of $11.9 million each. William McGuire, former CEO of United Healthcare, collected $1.3 Billion during his 15-year tenure. All this money comes right out of the outrageous premiums paid by policy holders and from the medical services denied them. Meanwhile, the head of the federal government’s Centers for Medicare & Medicaid Services (CMS), who manages healthcare for 87 million elderly, disabled and low-income people, gets paid just under $200,000. Illustration and commentary courtesy of Connect the Dots USA |

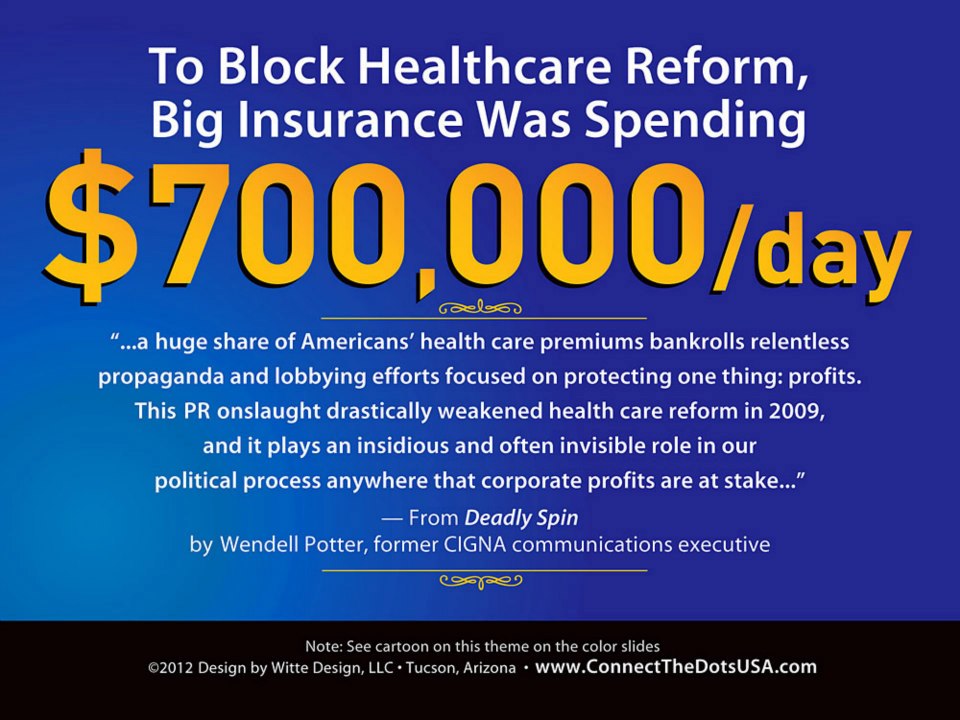

Big Insurance was spending $700,000 per day to fight reform and maintain the profits-over-people status quo. Using front groups and propaganda techniques ripped straight from the tobacco-industry’s playbook, they whipped uninformed masses into a hysteria about mythological death panels, government bureaucrats, socialism and the demise of freedom — the same old lies they trotted out when Medicare was being debated in the 1960s. Just as cigarette makers used to warn smokers that the nanny state was trying to take away their “freedom torches” or that cigarettes were the “healthy alternative to sweets,” Big Insurance and Big Pharma don’t give a hoot about your health or freedom — only their relentless pursuit of profits.

Illustration and commentary courtesy of Connect the Dots USA |

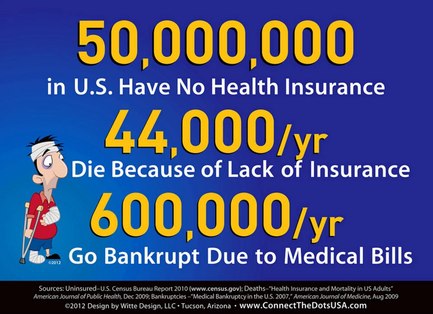

All this dysfunction has lead to some pretty shameful results for the U.S. healthcare system. As I mentioned, 50 million (16% of the U.S. population) have no health insurance. 81% of the uninsured (40.5 million) are U.S. citizens; the other 19% (9.5 million) include both legal residents and undocumented immigrants. Those without insurance often delay getting care until they are really sick and end up in the ER. This delay results in the preventable deaths of 44,000 uninsured adults under 65. That’s 15 times more than the deaths in the 9/11 tragedy every year. Where are all the self-proclaimed “pro-lifers” screaming about these deaths? Finally, 62% of all bankruptcies — 600,000 families in 2007 — are due at least in part to medical bills. And whatever costs these families still can’t pay get shifted to the rest of us. In no other developed country in the world do people die or go bankrupt because of lack of health insurance or access to care.

Illustration and commentary courtesy of Connect the Dots USA |

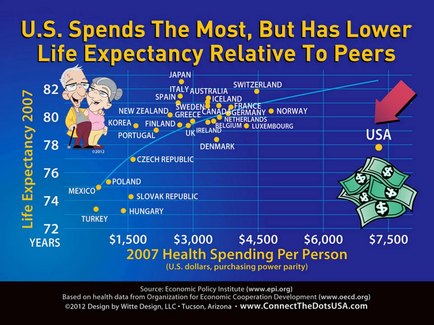

The average life expectancy in the U.S. is just under 78 years (even less if you’re a blue-collar worker). Meanwhile Japan’s average life expectancy is more than 82 years, and they spend less than half of what we spend on healthcare per person. The 2000 World Health Organization Report, which compared all the world’s 191 healthcare systems on a number of different measures, ranked the U.S. 37th in the world -- lower than Colombia and Costa Rica. In terms of “fairness of distribution,” the U.S. ranked 32nd; and on “fairness of financial contribution,” we ranked 54th. The best scorecards went to the health care systems in Japan, France, Germany and Sweden. A 2001 Harvard study measuring patient satisfaction found only 40% of Americans were satisfied with their health care system compared to Denmark’s 91% and Finland’s 81%. Let’s face it folks: We’re getting a Pinto healthcare system at Ferrari prices.

(Ferrari/Pinto metaphor by Joshua Holland, The Fifteen Biggest Lies About The Economy, p. 130) Illustration and commentary courtesy of Connect the Dots USA |

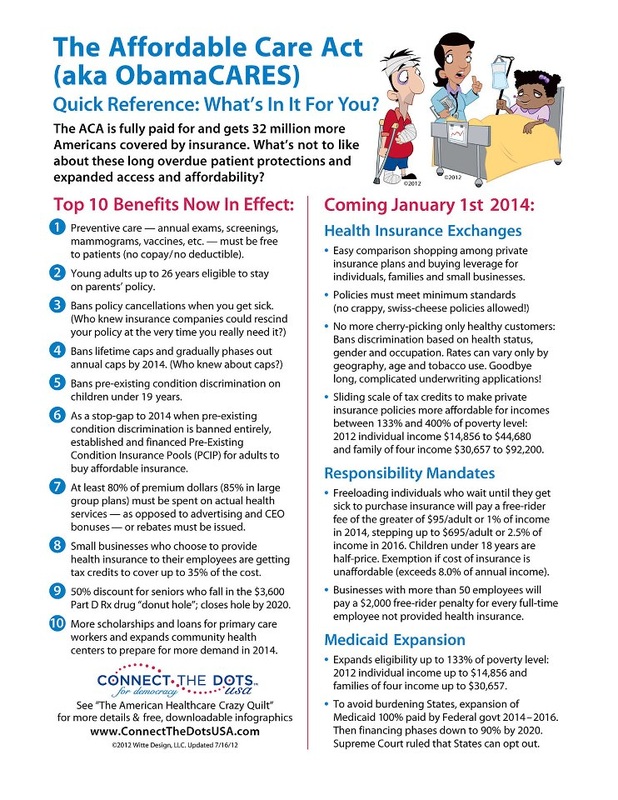

Towards that end, Obama and the Democrats after a year-long battle passed the Patient Protection & Affordable Care Act in March 2010 — aka the ACA or ObamaCARES. While it sometimes seems like a bunch of band-aids on a sucking chest wound, Obama succeeded in passing comprehensive healthcare reform where Roosevelt, Wilson, Truman, Nixon and Clinton had previously failed. Two years later, lots of folks don’t know all the good stuff that’s in it. Let’s start with the top 12 benefits already in effect and ask yourself “What’s not to likey?” First, the ACA requires that all policies cover preventive services like annual exams,

mammograms and vaccines with no co-pays or deductibles. Millions of young adults under age 26 are able to stay on their parents policies even if they are out of school and have a job. Next, it bans the unconscionable practice of cancelling policies when you get sick. Similarly, it bans those lifetime caps, gradually phases out annual caps by 2014, and bans pre-existing condition denials for children under 19 years. As a bridge to 2014, when pre-existing condition discrimination goes away for everyone, the ACA created Pre-Existing Condition Insurance Pools (PCIP). Illustration and commentary courtesy of Connect the Dots USA |

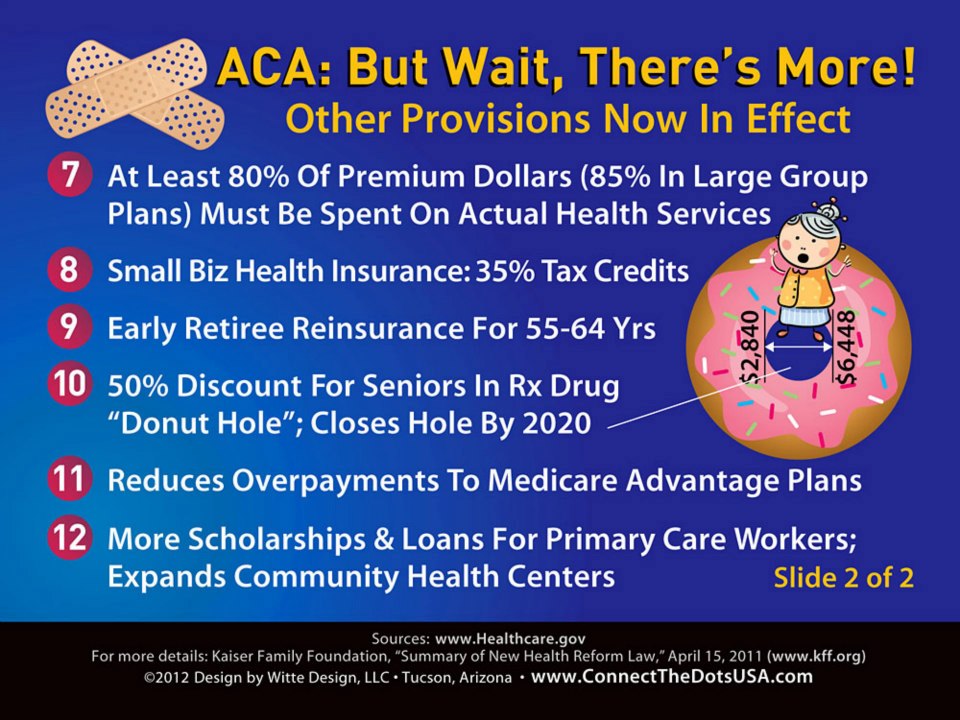

Next, insurance companies will have to spend 80% of premium dollars (85% in large group plans) on actual medical services or they must issue rebates to customers and could be blocked from selling in the health exchanges that go up in 2014. Over $1 Billion in rebate checks just went out this summer. Many small business who provide health insurance to their employees are getting tax credits of up to 35% of costs. The Early Retiree Reinsurance Program funded with $5 Billion was available to corporations to help offset premiums for pre-Medicare retirees. Medicare Part D has a notorious, goofy donut hole where seniors have to pay 100% of drug costs once they hit $2,800 until $6,400 in a given year. The ACA gives seniors a 50% discount on brand name drugs in the donut hole and gradually closes the hole by 2020. To extend Medicare’s Part A Trust Fund solvency to at least 2024, the ACA gradually reduces those overpayments to Medicare Advantage plans so private insurance companies will get the same as what Original Medicare pays by 2017. Instead, the law provides bonus payments for high quality overall care and cracks down on a lot of Medicare waste and fraud by doctors, hospitals and other providers. Finally, in preparation for millions more getting insurance starting in

2014, the ACA funds scholarships and loans to ramp up our primary care workforce, as well as expanding community health centers. Illustration and commentary courtesy of Connect the Dots USA |

The best parts comes January 1st, 2014. Each state is required to set up a web-based health insurance exchange where companies compete for your business and provide easy-toread, standardized comparison shopping. States that fail to set up their own will get a federal format. All policies sold must meet minimum standards so you can be confident you’re not getting a crappy, swiss-cheese policy full of holes. The exchanges are designed to give individuals, families and small businesses the group buying leverage they currently lack. And best of all, there will no longer be any discrimination based on pre-existing conditions health status, gender or occupation. Rates can only vary by geography, age (3:1 from oldest to youngest) and tobacco use (1.5:1). Fifteen-page underwriting applications will be a thing of the past. Hooray for ACA!

Illustration and commentary courtesy of Connect the Dots USA |

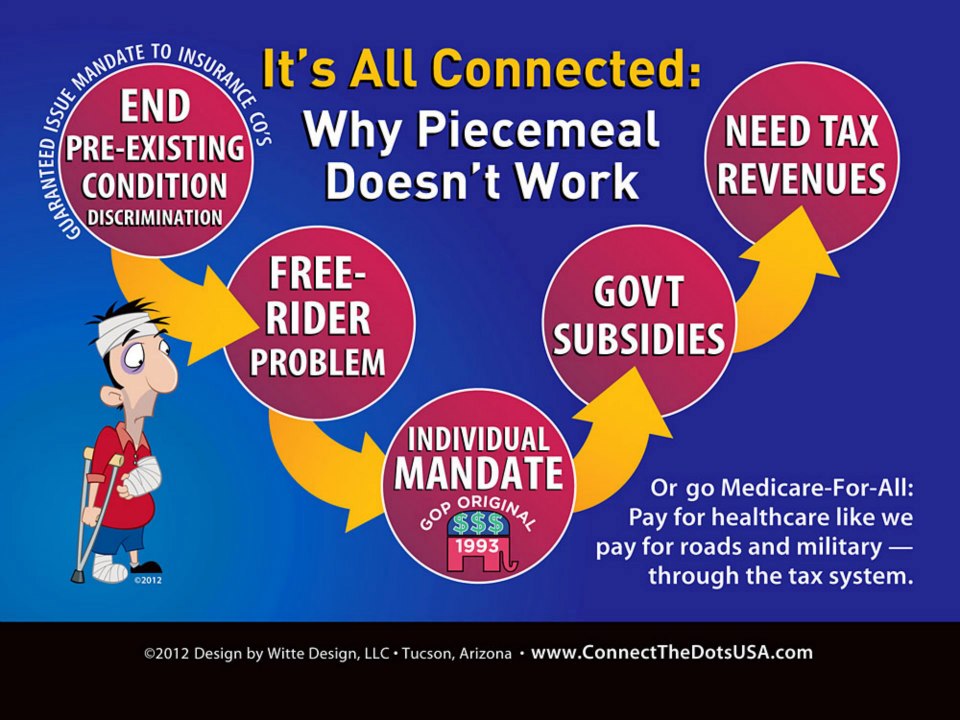

But if we mandate that the insurance companies stop cherry-picking only healthy people and accept everyone regardless of pre-existing conditions, then we create a free-rider problem. Rational individuals will just wait until they get sick and then sign up for insurance in the ambulance on the way to the hospital. Insurance pools don’t work if only sick people pay in. To prevent this moocher problem, it was actually Republicans who invented the individual mandate to buy health insurance back in 1993 as an alternative to Clinton’s proposed employer mandate. I mean doesn’t it just smell like a righty anti-parasite idea? So the motivation for the individual mandate is not the nanny state but rather the free market. Because some folks won’t be able to afford expensive private insurance no matter how much we require it, we’ll need to provide some government subsidies to make it more affordable. And then we’ll have to collect some tax revenues so these subsidies don’t add to the deficit.

Illustration and commentary courtesy of Connect the Dots USA |